Outstanding Cash Basis Accounting Spreadsheet

Accounting Spreadsheets For Small Business Daily Itinerary Template Excel Agenda 2018

Excel Cash Book For Easy Bookkeeping Keeping Templates Tutorials Workout Journal Gantt Timeline

Accrual To Cash Conversion Excel Worksheet Double Entry Bookkeeping Calculator Sales Forecast Template Staff Training Record

Daily Cash Sheet Template Download Free At Http Www Xltemplates Org Balance Bookkeeping Templates Excel Monthly Budget Checklist League Fixture Generator

Cash Basis To Accrual Conversion Example Showing Actual Calculations Required Spreadsheet Template Business Financial Plan Worksheet It Audit Excel Memo

Bookkeeping Spreadsheets For Excel Business Spreadsheet Template Google Docs Time Tracking Sheet Expenses

Accrual accounting by comparison records debit and credit transactions in five different account categories.

Cash basis accounting spreadsheet. You record expenses when cash is paid. In this method each item on an income statement is converted directly to a cash basis and each cash effect is directly reported. You own a variety store.

The cash basis involves only recording transactions when the. The cash flow statement helps you look back over a specific period typically a quarter to predict the net cash or amount of cash you will need over a specific accounting period to fund your operating activities. With cash basis accounting you record revenue when physical cash is received not when a transaction takes place.

When cash flows are more volatile but predictable cash budget is prepared more frequently even on a day today basis. Using accrual accounting and cash disbursement journals. First lets take a closer look at what cash flow statements do for your.

Many small businesses opt to use the cash basis of accounting because it is simple to maintain. The accrual basis of accounting is used to record revenues and expenses in the period in which they are earned irrespective of the timing of the associated cash flowsHowever there are times usually involving the preparation of a tax return when a business may instead want to report its results under the cash basis of accounting. The ending cash balance is the cash balance in the budgeted or pro forma balance sheet.

A cash budget template is a budget based on actual inflows and outflows of cash as opposed to being based on accounting principles such as revenue recognition Revenue Recognition Principle The revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a companys matching and. Cash flow should not be confused with profit. In financial accounting a cash flow statement provides a snapshot of your cash balance.

The direct method for calculating this flow involves deducting from cash sales only those operating expenses that consumed cash. This equation sets the foundation of double-entry accounting and highlights the structure of the balance sheet. Using this system in a nonprofit for example means youd record the payment when you receive a member or donors payment.

Free Cash Flow Statement Templates Smartsheet Template Warehouse Management System Excel Accounting For Small Business

Download Free Cash Book Template In Microsoft Excel Xltx File For Easy Maintenance Of Templates Spreadsheets Bookkeeping Client List Google Sheets Sheet Gantt Chart

Profit Loss Report Spreadsheet 7 0 Screenshot Small Business Accounting Finance Tax Raw Material Stock Format In Excel Daily Status Template

Cash Flow Statement Template Balance Sheet Excel Free Download Case Management Spreadsheet

Cash Flow Worksheet Monthly Microsoft Excel Organizer Statement Budgeting Worksheets Budget Recruitment Tracker Xls Spreadsheet For Trucking Company

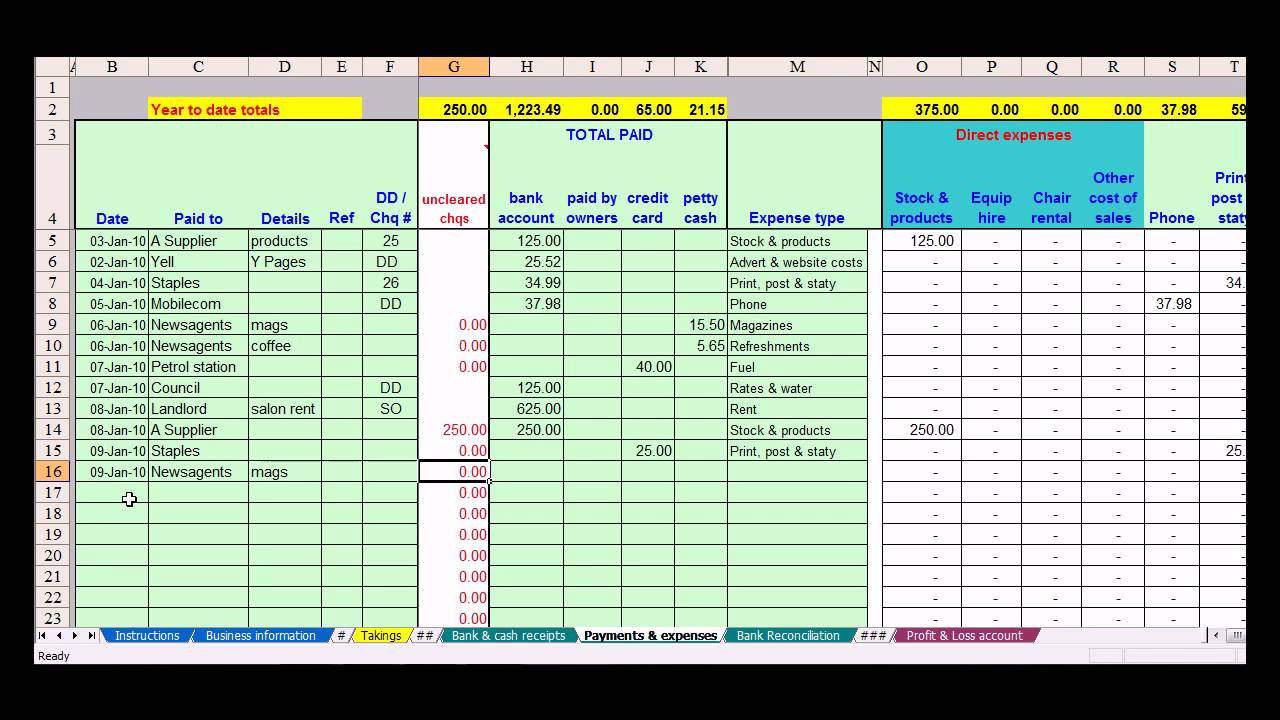

Hairdresser Bookkeeping Spreadsheet Templates Small Business Template Mileage Log Google Sheets Start Up Costs Worksheet

Simple Spreadsheets To Keep Track Of Business Income And Expenses For Tax Time All About Planners Spreadsheet Budget Excel 12 Month Calendar Creating A Tracker In

Daily Cash Sheet Template Bookkeeping Business Printables Small Organization Google Spreadsheet Contacts Excel Invoice System